Qualcomm has announced a diversification strategy that clearly outlines where it wants to take the company over the next three to five years. Historically linked to mobile devices and connectivity licensing, the manufacturer aims to strengthen its presence in automotive, Internet of Things, and especially data centers for artificial intelligence. The company sees several inflection points during this period and sets an ambitious goal: exceeding $18 in non-GAAP earnings per share in fiscal year 2029.

This financial message is significant because Qualcomm has been trying for years to convince the market that it can reduce its reliance on smartphones. Its Snapdragon chips remain essential for premium mobile devices and connected gadgets, and its licensing business continues to be highly profitable. However, future growth can no longer depend solely on phone refresh cycles. Artificial intelligence has opened a different opportunity: leveraging its expertise in low power, connectivity, and system design within data centers.

The company is not talking about vague diversification. In recent days, it has made a series of announcements outlining a broader strategy: acquiring Modular to bolster AI software, expanding collaboration with Hugging Face for open models from device to cloud, a multigenerational agreement with Meta for data center CPUs, and unveiling the Dragonfly family for AI infrastructure.

The financial goal: more than $18 in non-GAAP EPS in 2029

Qualcomm has set its non-GAAP earnings per share target for fiscal year 2029 above $18, compared to a GAAP diluted EPS goal of over $14.50. The company clarifies that the difference between these metrics mainly stems from stock-based compensation.

| FY2029 Target | Communicated Goal |

|---|---|

| GAAP diluted EPS | >14.50 $ |

| Non-GAAP diluted EPS | >18.00 $ |

| Timeline | FY 2029 |

| Guidance date | 06/24/2026 |

| Main non-GAAP adjustment | Stock-based compensation |

This figure should not be read as a guaranteed forecast. Qualcomm dedicates much of the statement to reminding that its objectives are subject to significant risks: dependence on a small number of customers, exposure to China, US-China tensions, vertical integration of clients, technological competition, supplier reliance, acquisitions, intellectual property litigation, regulation, semiconductor industry cycles, and macroeconomic volatility.

Even so, the financial target is meaningful because it shows how the company intends to reposition itself to investors. Qualcomm aims for the market to stop viewing it solely as a company tied to the mobile cycle and instead see it as a computing platform for AI, automotive, edge, and data centers.

Data centers: the new piece of the story

The most transformative announcement is Qualcomm’s serious entry into data centers. The company revealed Dragonfly, a family including the Dragonfly C1000 CPU, inference accelerators AI200, AI250, and AI300, High Bandwidth Compute technology, advanced connectivity, and custom silicon for large clients.

The focus is clearly on inference and AI agent workloads. Qualcomm believes that growth driven by AI agents will significantly increase token demand and that the key metric will be performance per watt. In other words: delivering more responses, actions, and AI flows with less energy and lower total cost.

This thesis aligns with its historical strengths. Qualcomm has built its position over decades designing efficient chips for devices operating under thermal and energy constraints. Now, it’s trying to transfer that experience to data center racks, where electricity, cooling, and efficiency are critical financial variables.

| Business Area or Technology | Role in Diversification |

| Snapdragon | Mobile, PCs, and personal devices |

| Dragonwing | Edge, IoT, industrial, automotive, and connected systems |

| Dragonfly | Data centers and AI infrastructure |

| Modular | Software, portability, and efficient model deployment |

| Hugging Face | Community, open models, and development flow |

| Meta | Key client for data center CPUs |

The partnership with Meta for Dragonfly C1000 CPUs is particularly significant. Qualcomm expects its first generation of data center CPUs to be in production by mid-2028 and to support Meta’s future capacity expansions. For a strategy that still needs to demonstrate execution, having Meta as a customer provides strong commercial validation.

The Modular acquisition changes the hardware narrative

Qualcomm recognizes that silicon alone isn’t enough. In AI, adoption depends equally on software and chips. NVIDIA has built its advantage around CUDA, libraries, frameworks, tools, and community. If Qualcomm wants to compete in inference, edge, and data centers, it needs a software layer that facilitates porting and optimizing models on heterogeneous hardware.

The acquisition of Modular aligns with this goal. Modular develops tools to run AI models across different architectures—from CPU and GPU to NPU and custom ASICs. The company also promotes Mojo, a performance-oriented language with familiar syntax for Python developers.

For Qualcomm, Modular can become the bridge between its hardware and developers. The expanded partnership with Hugging Face adds distribution: over 16 million developers and more than 3 million open models within an ecosystem already used by industry for experimenting, sharing, and deploying AI.

The approach is clear. Qualcomm buys software, engages with the open models community, introduces data center hardware, and secures relevant customers. The goal is to create a comprehensive platform, not just sell standalone components.

Why diversification is urgent

Qualcomm still has a large mobile business but faces structural risks. The company acknowledges in its regulatory disclosures its dependence on a limited number of clients and licensees, especially in premium devices. It also mentions risks of vertical integration by customers, a sensitive point in a market where Apple, Google, Samsung, and others increasingly design their own components.

Exposure to China adds another layer of uncertainty. Qualcomm derives a significant portion of its revenue from that market, and US-China trade and national security tensions could impact sales, licensing, customer access, or supply chains. For investors, diversifying revenue streams isn’t just an opportunity for growth; it’s also a way to reduce concentration risk.

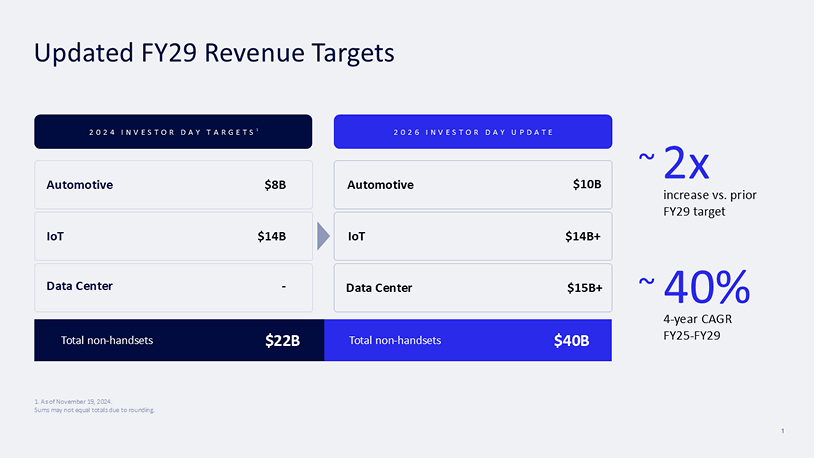

Automotive and IoT have been part of this narrative for years. The new development is that data centers have shifted from a challenging aspiration to a much more concrete commitment. AI has expanded the accessible market size and opened gaps for alternative architectures, especially as customers seek to cut energy costs and reliance on dominant suppliers.

| Traditional Qualcomm Risks | Strategic Response |

| Dependence on smartphones | Expansion into automotive, IoT, PCs, and data centers |

| Concentration on few clients | New agreements with hyperscalers and AI companies |

| Vertical integration pressure | Custom silicon and comprehensive platforms | Dependence on China | Greater presence of global infrastructure clients |

| Semiconductor competition | Differentiation through performance per watt and software |

| Dominance of rival ecosystems | Modular, Hugging Face, and developer-driven strategy |

The opportunity: distributed AI and token cost

The most intriguing aspect of Qualcomm’s strategy is in distributed AI. The company aims not to limit itself to data centers or devices alone. Its thesis is that many AI workloads will be distributed among mobile, PC, automotive, industrial edge, and cloud. Some tasks will run locally for privacy or latency reasons; others will go to data centers due to complexity; and some will dynamically shift based on cost, performance, and availability.

This approach could be appealing to companies that don’t want to rely solely on large closed APIs. It also fits open models, local inference, and agents operating across multiple systems. Qualcomm seeks to place its platforms throughout this continuum: Snapdragon in devices, Dragonwing at the edge, and Dragonfly in data centers.

The underlying financial metric is cost per token. If infrastructure can process more tokens per watt, inference costs decrease. And if costs drop, more AI applications become commercially viable. Qualcomm wants to convince clients and investors that its low-power DNA gives it an edge in this new economy.

Risks: schedule, competition, and execution

While the strategy is coherent, the schedule warrants caution. Dragonfly C1000 won’t reach production until mid-2028. Significant data center revenue will depend on technical validation, manufacturing, customer integration, software availability, deployment in actual racks, and competition from more established players.

NVIDIA not only dominates AI accelerators; it also controls much of the software and system architecture. AMD competes with EPYC and Instinct. Intel maintains a presence in servers. Amazon, Google, and Microsoft develop their own CPUs and accelerators. Broadcom and Marvell are gaining prominence with custom ASICs. Qualcomm enters a race against well-established rivals and demanding clients.

There’s also a risk related to integration. Acquiring Modular can accelerate the strategy, but maintaining a startup culture within a large semiconductor company isn’t always easy. Additionally, Hugging Face is an open and neutral ecosystem; Qualcomm will need to avoid perceptions of trying to close or bias that environment toward its own hardware.

From a financial perspective, the 2029 goals depend on several assumptions: refresh cycles, AI adoption, new clients, expansion into automotive and IoT, acceptance of Dragonfly, geopolitical stability, and successful acquisitions. Qualcomm can have multiple inflection points but also face several failure points.

What investors should watch

The first indicator will be the conversion of deals into revenue. The agreement with Meta validates the roadmap, but products won’t immediately reach volume. Investors should monitor firm order commitments, schedules, manufacturing partners, system availability, and independent performance benchmarks.

The second will be margins. Entering data centers can open new revenue streams but also requires significant R&D, software, support, and supply chain investment. The question is whether Qualcomm will maintain attractive margins while competing in a highly aggressive market.

The third is the balance between hardware and software. Modular and Hugging Face can make Qualcomm’s story more convincing to developers. If deployment experiences are positive, adoption may accelerate. If software development lags, hardware may struggle to gain traction.

The fourth is the evolution of the mobile business. Diversification won’t instantly replace Snapdragon and licensing revenues. For years, mobile will continue to fund much of Qualcomm’s investments. If the smartphone market weakens or a key customer reduces dependence on Qualcomm, the transition could become more difficult.

Qualcomm’s new valuation game

Qualcomm’s ambition is clear: to stop being seen as a mobile-focused company with adjacent businesses and become a computing platform for the AI era. If successful, its growth profile and valuation could change significantly. If not, the market may continue to apply the usual discount associated with company exposure to smartphone cycles and concentration risk.

The presented strategy is more substantial than previous attempts because it combines several components: key clients like Meta, software via Modular, community through Hugging Face, Dragonfly hardware, Edge with Dragonwing, and an explicit financial target for 2029. The true test, however, will be execution.

AI is compelling all major semiconductor players to redefine themselves. Qualcomm has a real opportunity because the market is no longer limited to training giant models in a few data centers; inference, more agents, more connected devices, and increased demand for efficiency are the new realities. This aligns with its technical heritage.

The question remains whether Qualcomm will arrive in time and with a sufficient ecosystem. The AI market moves very fast, and infrastructure clients won’t buy promises for long. They buy performance, costs, support, and availability. From now on, Qualcomm will need to show that Dragonfly isn’t just an attractive roadmap but a real, competitive platform ready for production.

Frequently Asked Questions

What is Qualcomm’s financial target for 2029?

Qualcomm aims for a non-GAAP diluted EPS exceeding $18 in fiscal year 2029, compared to a GAAP target of over $14.50.

Why does Qualcomm want to diversify beyond mobile?

Because its mobile business remains profitable but faces structural risks. It depends on a small number of clients, faces vertical integration pressures, and geopolitical risks. Automotive, IoT, and data centers offer new avenues for growth.

What role does Dragonfly play in the strategy?

Dragonfly is Qualcomm’s new family of solutions for AI data centers, including CPUs, inference accelerators, HBC technology, connectivity, and custom silicon.

What is the biggest risk to the strategy?

Execution. Qualcomm must turn agreements and roadmaps into real products with mature software, active customers, and performance competitive with NVIDIA, AMD, Intel, and hyperscaler chips.

via: qualcomm