Italy does not appear in the global semiconductor landscape at the same level as Taiwan, South Korea, the United States, or the Netherlands. It also doesn’t compete with Germany or France across all industrial fronts in the sector. However, reducing its role to a marginal position would mean losing a significant part of the European picture: the country combines power manufacturing, analog electronics, research, test equipment, wafers, design, and now also advanced packaging.

Its economic size remains limited. According to the overview published by Elettronica e Mercati, the value of Italy’s semiconductor production is around $3-4 billion, while the entire supply chain—including equipment manufacturers, substrates, materials, and research centers—ranges from $6-8 billion. This figure is modest compared to the global market, but sufficient to position Italy as a specialized node within Europe’s chip strategy.

Timing is crucial. The EU Chips Act has accelerated public aid, national plans, and the pursuit of technological autonomy. Europe aims to gain influence in semiconductors, but it cannot do so by copying the Taiwanese or South Korean models from scratch. Its real margin lies in reinforcing areas where it already has capacity: automotive, power, analog, sensors, machinery, packaging, research, and industrial applications. Italy fits precisely within that logic.

Catania and Silicon Carbide: The Major Industrial Bet

The most significant project is in Sicily. STMicroelectronics will invest about €5 billion in Catania to develop an integrated silicon carbide campus, with approximately €2 billion in Italian public support approved by the European Commission. The facility will produce power devices and modules based on SiC, an essential technology for electric vehicles, renewable energies, industrial systems, and advanced electrification.

Production is scheduled to start in 2026, with full capacity expected by 2033. ST talks about up to 15,000 wafers weekly once the project is fully operational. For Italy, the importance is not only in volume. Silicon carbide is one of the areas where Europe can compete more sensibly because it is closely linked to industrial sectors where the continent retains influence: automotive, energy, electrical grids, industry, and transportation.

| Project | Location | Investment | Public Support | Goal |

|---|---|---|---|---|

| STMicroelectronics SiC Campus | Catania, Sicily | €5 billion | €2 billion | Integrated SiC production |

| Planned Production | Catania | Starting 2026 | — | Devices and power modules |

| Full Capacity | Catania | By 2033 | — | Up to 15,000 wafers weekly |

| Main Uses | Automotive, renewables, industry | — | — | Electrification and energy efficiency |

Catania does not start from zero. The so-called Etna Valley has been linked to STMicroelectronics and power electronics for years. The company already produces SiC devices there and has lines related to GaN and RF technologies. This industrial continuity is an advantage: semiconductor projects need talent, suppliers, universities, technical centers, and accumulated experience.

Italy, at this point, is not aiming to lead in the most advanced 2 or 3 nanometer nodes. Instead, it seeks strength where value does not solely depend on extreme lithography but on materials, reliability, vertical integration, energy efficiency, and industrial applications. Italy aligns with this approach.

Novara and the Shift Toward Advanced Packaging

The second major move is in the north. Silicon Box, a Singapore-based company specializing in advanced packaging, will invest €3.2 billion in a packaging and testing plant in Novara, Piedmont. The project has about €1.3 billion in public support approved by Brussels and plans to create around 1,600 qualified jobs.

Advanced packaging has become a central piece of the industry. As chips are designed with chiplets and high-bandwidth memory, manufacturing good dies is no longer enough. They must be integrated into increasingly complex modules. Packaging has shifted from a final assembly phase to a technical element that influences performance, power consumption, cost, and scalability.

| Project | Company | Location | Investment | Planned Jobs |

| Advanced Packaging Plant | Silicon Box | Novara, Piedmont | €3.2 billion | 1,600 jobs |

| Public Support Approved | Italy / EU | Novara | €1.3 billion | — |

| Primary Activity | Silicon Box | Packaging, testing, integration | — | Chiplets and advanced modules |

For Italy, Silicon Box’s arrival opens a different door from traditional manufacturing. The country already has wafer production, test equipment, and design centers but lacked an advanced packaging facility on this scale. If executed as planned, Novara could become an important hub for European clients needing to integrate complex chips without relying entirely on Asia.

This move also has strategic significance. Europe has learned over recent years that manufacturing semiconductors involves more than just having fabs. It requires substrates, wafers, gases, equipment, testing, packaging, design, software, and skilled talent. An incomplete supply chain remains vulnerable.

STMicroelectronics as the System’s Core

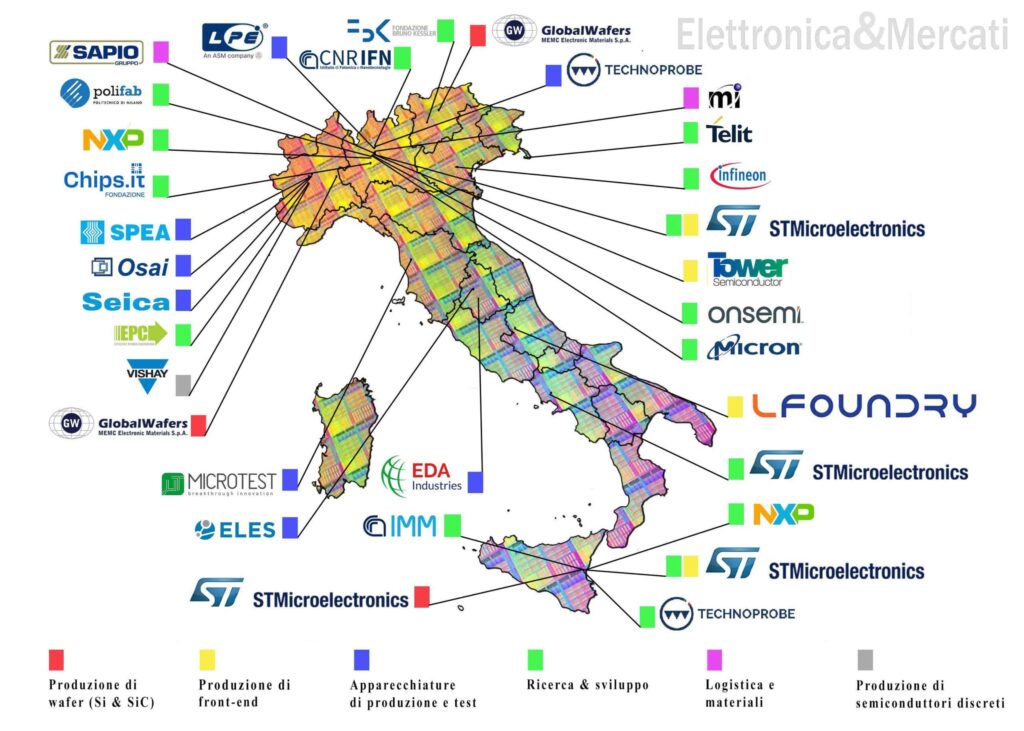

The heart of Italy’s industry remains STMicroelectronics. The Franco-Italian company maintains two major hubs in Italy: Agrate Brianza, near Milan, and Catania. In Agrate, it is completing its 300 mm R3 facility focused on power, analog, mixed signal, and RF chips. In Catania, it concentrates much of its SiC investments.

According to the Italian overview, ST employs over 12,500 people in Italy, with about 3,500 working in R&D. The company also runs R&D centers in various Italian cities, from Aosta and Bologna to Pisa, Naples, Lecce, Messina, and Palermo.

| Actor | Role in Italy |

| STMicroelectronics | Manufacturing, SiC, analog, power, RF, R&D |

| LFoundry | 200 mm foundry in Avezzano |

| Tower Semiconductor | Presence in part of ST’s R3 process in Agrate |

| MEMC / GlobalWafers | Wafer production in Merano and Novara |

| Technoprobe | Probe cards and semiconductor testing |

| Leonardo | MMIC in GaAs and GaN for defense and aerospace |

Another relevant manufacturer is LFoundry, based in Avezzano. Its history reflects some of the ups and downs of European microelectronics: founded under Texas Instruments, went through Micron, and ended up owned by Chinese interests. Today, it operates as a foundry with 200 mm lines and 110/150 nm technologies, specializing in areas like image sensors.

Italy also hosts MEMC Electronic Materials, controlled by GlobalWafers, with factories in Merano and Novara. The Novara plant is one of Europe’s large 200 mm wafer facilities, and GlobalWafers has invested to move toward 300 mm production. While less visible than a major fab, it’s a vital part of the supply chain.

Italy’s Strengths: Machinery, Testing, and Niche Industries

One of Italy’s most interesting features is the presence of companies specialized in test equipment, probe cards, gases, engineering, clean rooms, and services supporting fabs. While not as high-profile as TSMC or NVIDIA, they form the machinery backbone supporting chip production.

Technoprobe, headquartered in Brianza, is a clear example. The firm has become a global leader in probe cards, essential tools for testing chips during manufacturing. Besides, firms like SPEA, Seica, OSAI, Microtest, ELES, EDA Industries, and LPE (specialized in epitaxial reactors and acquired by ASM International) contribute heavily to the ecosystem.

| Area | Key Italian Companies |

| Probe cards | Technoprobe |

| Semiconductor testing | SPEA, Seica, OSAI, ELES, Microtest, EDA Industries |

| Epitaxial reactors | LPE / ASM International |

| Silicon wafers | MEMC / GlobalWafers |

| Process gases | Sapio, SIAD, and other suppliers |

| Engineering and clean rooms | Meridionale Impianti, Galvani, and specialized providers |

This specialization aligns with Italy’s industrial structure. The country doesn’t always compete by size but by applied engineering, machinery, automation, niche components, and highly technical supply chains. In semiconductors, this tradition can be more useful than it appears.

The Weak Spot: Few Fabless Companies

Italy’s main weakness lies in fabless design. While the US has built giants like NVIDIA, AMD, Qualcomm, or Broadcom based on a fabless model, Italy has few companies focused solely on IC design. This is a shortcoming shared partly with Europe but particularly visible in Italy.

Exceptions include INVENTVM, OPTOI, Microtest in ASIC design, and some startups and companies involved with sensors, microfluidics, UWB, or printed electronics. Still, there is no critical mass comparable to leading international centers.

This is where Fondazione Chips-IT comes in, the Italian national center for IC design, based in Pavia. Its goal is to bolster research, technological transfer, and chip design, connecting universities, research centers, and companies. For Italy, this may be the most important long-term step: without domestic design, the value captured in the supply chain is limited.

| Weakness | Italian Response |

| Poor fabless ecosystem | Establishing Fondazione Chips-IT |

| Limited global scale | Specialization in power, analog, and packaging |

| Dependence on external foundries | Strengthening local design, testing, and supply chain |

| Lack of specialized talent | Connecting with universities and research centers |

| Industrial fragmentation | Public funding and European projects |

Design influences much of a chip’s value. Manufacturing matters, but architectures, IP, software, validation, and adaptation to specific markets can generate higher margins and greater technological control. If Chips-IT succeeds in attracting researchers, companies, and industrial projects, Italy could improve its position in the most strategic part of the supply chain.

Public Funding and Technological Sovereignty

Italy has launched a national microelectronics fund to support research, pilot lines, and new industrial investments. According to Italian economic promotion, in 2022 the country started a dedicated fund for microelectronics within a broader strategy to advance the sector. Alongside the EU Chips Act, these tools are used to attract projects like ST in Catania or Silicon Box in Novara.

The question remains whether these investments are enough to change Italy’s scale. Probably not enough to turn Italy into a global chip giant, but they can reinforce a realistic position within Europe. In semiconductors, being strategic doesn’t always mean dominating every node; it can also mean becoming hard to replace in materials, power, packaging, testing, sensors, or industrial design.

Europe aims to increase its share of global semiconductor production to 20% by 2030. It is an ambitious and challenging goal. Italy can contribute by consolidating three areas: SiC and power in Catania, advanced packaging in Novara, and design and research around Chips-IT, universities, and tech centers.

Italy doesn’t start from scratch. It has a history—from Olivetti and SGS to STMicroelectronics. It has factories, wafers, testing, engineering, and R&D. It also has weaknesses: limited fabless scale, reliance on foreign fabs for advanced nodes, and a still-small global footprint.

The “Italy of Chips” won’t be the European Taiwan, nor does it need to be. Its opportunity lies in becoming a complete, specialized, connected industrial chain aligned with Europe’s needs: electric vehicles, renewables, power, sensors, defense, packaging, and applied design. In an industry where each country seeks its niche, this combination can be more valuable than trying to compete on all fronts simultaneously.

FAQs

What is Italy’s role in the semiconductor industry?

Its overall footprint is limited. Italian semiconductor production is around $3-4 billion, and the entire supply chain—including equipment, materials, substrates, and research—ranges between $6-8 billion.

What is Italy’s largest chip project?

One of the biggest is STMicroelectronics’ silicon carbide campus in Catania, with an investment planned around €5 billion and about €2 billion in public support.

What does Silicon Box in Novara contribute?

Silicon Box will build an advanced packaging and testing plant in Novara, with €3.2 billion in investment and about 1,600 skilled jobs.

What is Chips-IT?

Fondazione Chips-IT is Italy’s national center for IC design. Its aim is to strengthen Italy’s capabilities in design, research, and tech transfer.