Digi has for the first time detailed the architecture of its fiber backbone network in Spain. The information appears in its 2025 annual report and provides insight into how the core of an infrastructure that already passes through approximately 13.7 million homes is organized. It combines its own FTTH network with the SOTA network and also relies on wholesale agreements in certain areas.

This data matters because Digi has ceased to be just a price-driven operator. Its fiber deployment, its shift to a Mobile Network Operator (MNO) since January 2025, and its long-term agreement with Telefónica paint a picture of a company building a much more structural position in the Spanish market. Publishing the backbone map helps to shape this strategy: 14,000 kilometers of intercity backbone fiber and, according to a visual count from the map itself, 52 main nodes or core routers distributed across the country.

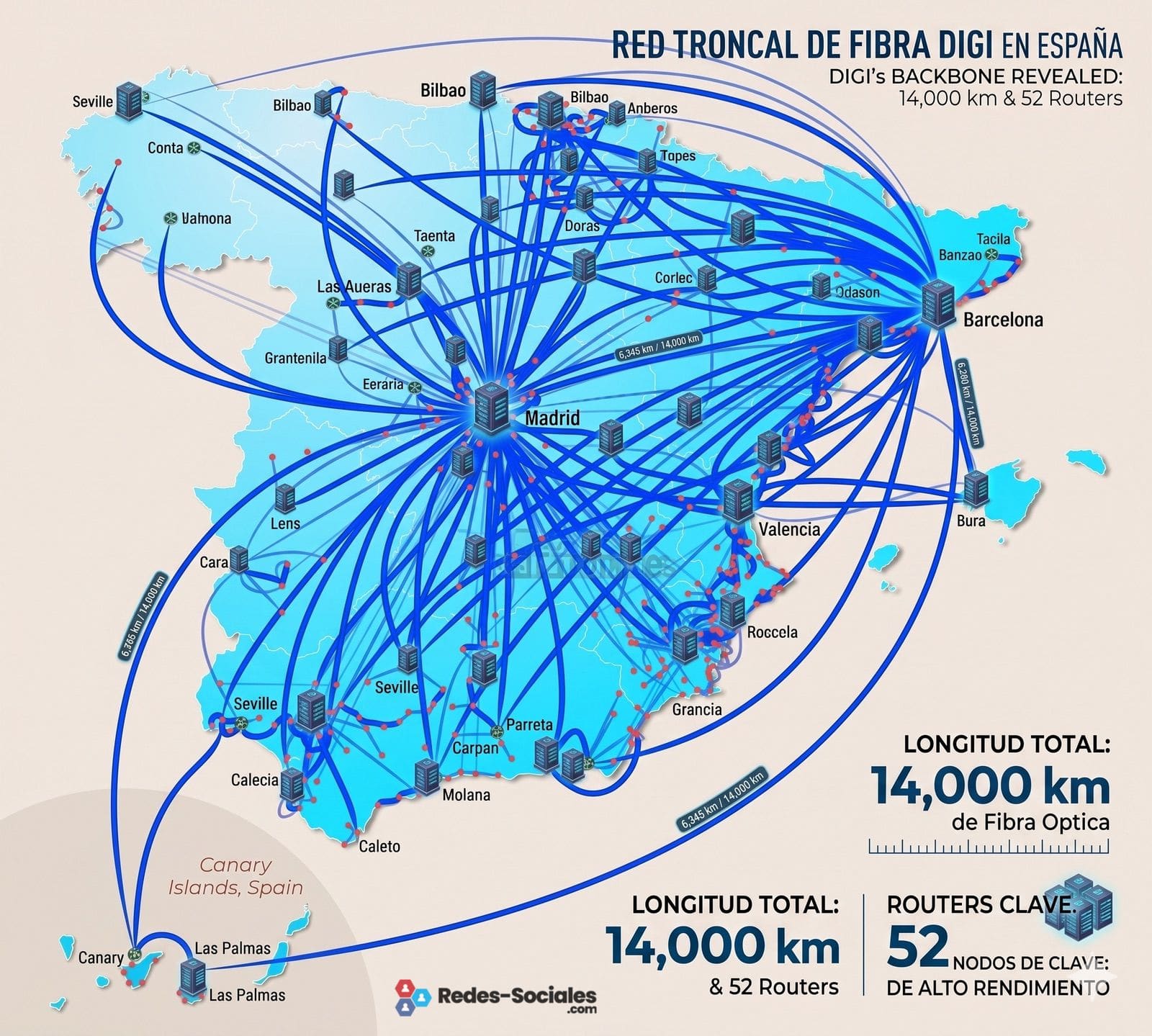

A map showing how the Smart network is maintained

Until now, Digi has published figures on fiber coverage, homes passed, and commercial growth, but had not shown with this level of detail the backbone infrastructure in Spain. The map included in the annual report represents the backbone links connecting the main localities where its fixed network operates.

In the image, nodes are visible almost throughout the mainland territory, with a concentration around Madrid, Barcelona, and major connectivity corridors. The blue lines display the backbone fiber connections between points of presence. Green icons appear to correspond to core routers, while red points could represent central offices, fiber headends, or technical sites associated with the access network. Digi does not explicitly detail the exact function of each symbol, so this interpretation is a technical reading of the map.

What the company does confirm in the report is that in Spain it provides fixed Internet and fixed telephony services through an FTTH network primarily built with XGS-PON technology, along with the SOTA network, which it accesses via a consortium led by Macquarie Capital. Together, they serve around 13.7 million homes, with a penetration rate of 15.8%. Additionally, Digi reports an intercity backbone network of approximately 14,000 kilometers.

| Published or deduced data | Digi’s situation in Spain as of 12/31/2025 |

|---|---|

| Intercity backbone fiber | 14,000 km |

| Homes passed by fixed and SOTA networks | 13.7 million |

| Coverage over country’s housing stock | 51.3% |

| Penetration over homes passed | 15.8% |

| Identifiable core routers on the map | 52, based on visual count |

| Predominant FTTH technology | XGS-PON |

| Fixed services | Internet, fixed telephony, and IPTV |

| Additional wholesale support | NEBA over Telefónica’s network in certain areas |

The backbone network is the least visible part for the customer, but one of the most vital. It connects cities, transports aggregated user traffic, links to interconnection points, and sustains both fixed and mobile services. In other words, passing fiber in front of buildings isn’t enough; a transport network capable of absorbing traffic, maintaining redundancy, and growing without degrading service quality is necessary.

Why the backbone alters the perception of Digi

For years, Digi has been perceived mainly as a price-competitive operator. That perception remains true but incomplete. The publication of the map reveals a deeper strategy: the operator is building a national transport network to gain independence, control costs, and improve its market position against more established competitors with greater infrastructure.

The difference between renting capacity and operating a backbone network of its own is significant. Those who control part of the backbone can better manage traffic, design routes, reduce dependency on third parties, and scale the network according to their own demand. They can also connect FTTH headends, metropolitan nodes, points of presence, and mobile sites more efficiently.

This is even more critical now that Digi operates in Spain as an MNO. Until January 2025, the company provided mobile services as a virtual operator over Telefónica’s network. Since then, it has used the National Roaming Agreement and the RAN and spectrum sharing agreement with Telefónica, valid until at least December 31, 2040. Additionally, Digi holds spectrum blocks in the 1,800 MHz, 2,100 MHz, and 3,500 MHz bands, acquired through conditions linked to its operation of Orange-MásMóvil.

| Network layer | Implication for Digi |

|---|---|

| Own FTTH | Greater control over fixed access and customer experience |

| SOTA network | Additional coverage in provinces where Digi sold its network but maintains access and operations |

| NEBA Telefónica | Capacity to offer services in areas without sufficient own coverage |

| 14,000 km backbone | National transportation for fixed traffic and growth support |

| Mobile agreement with Telefónica | National coverage and transition toward greater mobile integration |

| Own spectrum | Foundation to establish Digi as a network-based mobile operator |

The SOTA operation also helps explain Digi’s financial approach. The company sold part of its FTTH network to an investor consortium but retains access and operational responsibilities, allowing continued use of the infrastructure for service provision. In Andalusia, Digi completed the rollout of its FTTH network in October 2025, in collaboration with Aberdeen, reaching around 2.5 million homes passed.

The overall strategy is a hybrid one: own investment, agreements with infrastructure funds, wholesale access, and collaboration with Telefónica. It isn’t a purely owned network at every level, but it’s also not a lightweight virtual operator model. Digi is occupying an intermediate space—having more infrastructure control than typically attributed to low-cost operators.

Madrid and Barcelona as natural hubs

The map also shows what’s expected in a national network: Madrid and Barcelona act as major hubs. From these locations, routes branch out across the country, connecting to the north, Levante, Andalusia, Castilla-La Mancha, Castilla y León, Galicia, and the Ebro Valley. This structure aligns with the logic of national and international traffic, as both markets host data centers, interconnection points, key clients, residential traffic, and exits to global networks.

A technical reading should be approached cautiously because the report does not detail capacity, redundancy, transport providers, alternative routes, segment lengths, or logical topology. It also doesn’t specify whether all green nodes share the same function or if red points correspond to OLTs, headends, metropolitan hubs, or other sites. Nonetheless, the map offers a clear signal: Digi possesses an extensive and distributed backbone network, not just a presence limited to a few metropolitan areas.

Comparison with the community efforts by users reporting deployments of existing Smart fiber networks in forums and unofficial maps is also interesting. The overlap between cities with detected deployments and backbone points reinforces the value of this citizen tracking, even though the official source now better distinguishes confirmed details from inferences.

Impact on the Spanish market competition

This publication comes into a very concentrated Spanish market following the creation of MasOrange and amid competition between Telefónica, Vodafone, and Digi for fiber and mobile customers. In this environment, infrastructure has become one of the key variables separating operators capable of maintaining aggressive prices from those relying heavily on wholesale costs.

For Digi, having 13.7 million homes passed and 14,000 kilometers of backbone does not alone guarantee profitability or quality. The annual report notes that telecoms are capital-intensive, subject to competition, price pressures, technological changes, and ongoing investment needs. However, it helps explain why Digi’s growth in Spain shouldn’t be seen only as a sales campaign.

The operator finished 2025 with 10.8 million RGUs in Spain, including 7.3 million mobile and 2.6 million broadband. It also maintained the top position in mobile portability in Spain for the fifth consecutive year, according to the CEO’s message included in the annual report. These figures show that the company is no longer marginal in the market.

The now-visible backbone helps understand the next steps. If Digi wants to continue expanding its fiber, IPTV, mobile, business offerings, and convergent services, its transport infrastructure must support that growth. The published map is not just a technical curiosity; it’s a snapshot of the physical foundation on which the operator aims to capture a larger share of the Spanish market.

Frequently Asked Questions

What has Digi published about its network in Spain?

Digi has included in its 2025 annual report a map of its fixed backbone network in Spain, along with data on coverage, homes passed, and fiber length.

How many kilometers is Digi’s backbone network in Spain?

The company reports approximately 14,000 kilometers of intercity backbone fiber.

How many homes does Digi’s fixed network reach?

Digi states that its FTTH and SOTA networks together pass around 13.7 million homes, representing 51.3% of the country’s housing stock.

Is Digi already a mobile operator with its own network in Spain?

Since January 2025, Digi provides mobile services as an MNO through national roaming agreements, RAN sharing, and spectrum sharing with Telefónica. It also uses owned spectrum in several bands.

via: Digi Annual Report