NVIDIA has become the company that best encapsulates the AI economy. Its GPUs power hyperscale data centers, its systems define much of the training and inference infrastructure, and its software remains a formidable competitive advantage. However, the stock debate has shifted: the market no longer questions whether NVIDIA is an extraordinary company, but rather how much growth it can continue to generate now that its market cap exceeds $5 trillion.

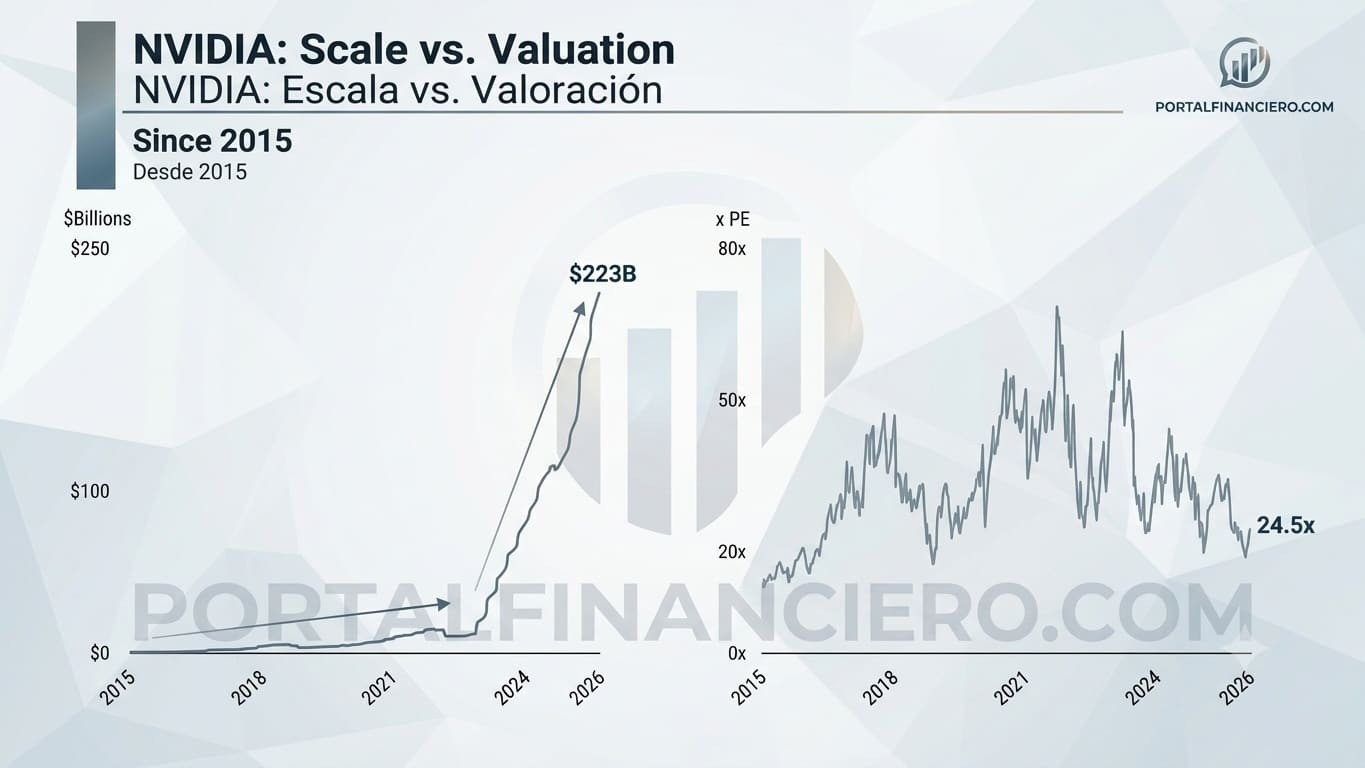

The emerging thesis among tech investors is provocative: NVIDIA doesn’t have a valuation problem; it has a size problem. According to market data from 05/19/2026, the company’s market capitalization was around $5.4 trillion. Based on an estimated profit of $223 billion, this valuation implies a multiple close to 24.5 times future profits—far from the multiples historically granted to small, hyper-growth companies.

Mathematics becomes uncomfortable

The calculation is simple—and precisely because of that, uncomfortable. With an estimated profit of $223 billion, NVIDIA is worth about $5.5 trillion if the market applies a 24.5x multiple. But if it traded at 50 times profits, its market cap would surpass $11 trillion. At 70 times, it would exceed $15 trillion.

| Estimated Profit | Applied Multiple | Theoretical Market Cap |

|---|---|---|

| $223 billion | 24.5x | $5.46 trillion |

| $223 billion | 50x | $11.15 trillion |

| $223 billion | 70x | $15.61 trillion |

This is the implicit message from the market: it doesn’t seem to be saying NVIDIA will earn little money. Instead, it’s offering a nuanced perspective: “I believe you’ll earn a lot, but I’m not willing to pay as if that pace could last indefinitely.”

Comparing this situation to a startup can help clarify the issue. A small company can double its revenue over several years if starting from a modest base. NVIDIA no longer plays in that league. It closed fiscal year 2026 with revenues of $215.9 billion, a 65% increase from the previous year, including $193.7 billion from Data Center. In the fourth fiscal quarter, it reported $68.1 billion in revenue, with a GAAP gross margin of 75.0%. These figures justify its leadership but also make it harder to sustain the growth rates typical of emerging companies.

The market doesn’t doubt the business, it doubts the cycle’s duration

The main bullish argument remains robust. Artificial intelligence is entering a phase of massive deployment: model training, large-scale inference, autonomous agents, generative video, robotics, simulation, semantic search, enterprise copilots, and scientific applications. Each of these demands more computing power, increased memory, better networking, and greater energy efficiency.

NVIDIA aims to capture this cycle with a comprehensive platform. Rubin, Vera, NVLink, Spectrum-X, BlueField, and their rack designs are intended to have the company sell not just GPUs but complete systems for “AI factories.” Its upcoming Rubin platform promises, according to NVIDIA itself, up to 10 times lower inference cost per token and up to four times fewer GPUs needed to train Mixture of Experts (MoE) models compared to Blackwell.

This point is critical for valuation. If NVIDIA manages to reduce the cost per token, it can expand the total addressable market. The agentic AI isn’t just about chatbot responses. An agent consults tools, executes code, uses sandboxes, retrieves documents, calls APIs, and maintains context over long processes. All of this increases token consumption and can turn inference into a market as large or larger than training.

However, the market also perceives risks. The first involves competition from NVIDIA’s own clients. Google has TPU, Amazon develops Trainium and Inferentia, Microsoft works with Maia, and other hyperscalers are exploring ASICs for workloads where NVIDIA GPUs might be overkill. They don’t need to replace NVIDIA entirely; it’s enough to shift some repetitive or mature workloads to proprietary silicon to improve costs and negotiate better terms.

The second risk pertains to margins. An extraordinary gross margin of 75% invites competition. The more NVIDIA earns per unit of AI infrastructure, the greater the incentive for clients and rivals to develop alternatives. The company can sustain these margins if its performance, software, and integration remain clearly superior. But if the market begins accepting solutions that are “good enough” for parts of inference tasks, pressure will mount.

The third risk involves the scale of investment in AI itself. Hyperscalers are spending enormous sums on data centers, energy, networks, and chips. If AI applications take longer than expected to generate economic returns, spending could pause or shift towards more efficient solutions. NVIDIA would still be essential, but the multiple the market is willing to pay might contract.

The real question: how much is the de facto AI monopoly worth?

NVIDIA has something few tech giants have achieved: an almost mandatory position in the most demanded infrastructure of the era. It’s not just hardware. It’s CUDA, libraries, networking, complete systems, developer communities, cloud integration, and a roadmap that compels the entire sector to respond.

Applying traditional multiples may be insufficient. If AI becomes a new global productive layer—akin to electricity, the internet, or cloud—NVIDIA could continue capturing value for many years. In such a scenario, the market is undervaluing the durability of its advantage.

But a company with a $5.4 trillion valuation can’t grow indefinitely without hitting physical limits. It needs advanced manufacturing capacity, HBM memory, packaging, energy, data centers, liquid cooling, customers with budgets, and profitable use cases. At this size, valuation depends not only on technological quality but also on the world’s capacity to absorb a tremendous amount of AI infrastructure.

The most reasonable answer probably isn’t at the extremes. The market might be justified in not paying 50 or 70 times estimated profits for a company of this size, because the margin for error becomes enormous. But it could also be underestimating the possibility that NVIDIA isn’t just a cycle-driven chipmaker but the provider of foundational infrastructure for the next decade of technology.

The debate will remain open as long as profits grow faster than doubts. If Rubin and Vera sustain the cost improvements per token and agentic inference turns into a mass load, NVIDIA might seem undervalued even at these valuations. Conversely, if hyperscalers begin migrating more loads to proprietary ASICs or AI spending moderates, the market’s valuation ceiling could be justified.

NVIDIA has already demonstrated it can build an extraordinary company. What remains to be shown is something more challenging: that a company weighing as much as a country can continue growing without the law of large numbers imposing limits. This tension, combined with the energy and infrastructure constraints already apparent across the sector, will define the next chapter of its valuation.

FAQs

Why is NVIDIA said to have a size problem?

Because its market cap is so large that maintaining very high growth rates requires enormous incremental profits. The market values not only its quality but also the difficulty of continued scaling.

Is NVIDIA cheap or expensive?

It depends on which future profit estimates are used as a reference. With very high profit estimates, the multiple might seem reasonable. The question is whether those profits can keep growing for many years.

What could drive NVIDIA’s valuation to $10 trillion?

Mass adoption of agentic inference, sustained AI spending growth, maintaining high margins, and continuous dominance of its platform over proprietary ASICs and alternatives from other providers.

What is NVIDIA’s biggest risk?

The combination of size, margin pressure, internal competition from hyperscalers, energy limits, and potential normalization of AI infrastructure spending.

Source: Portal Financiero