The second-hand semiconductor equipment market is gaining visibility amid the global race to boost chip manufacturing capacity. The reason is straightforward: opening or expanding a factory remains extremely costly, delivery times for many new tools are not always favorable for buyers, and a significant portion of the global business still relies on mature nodes, where reusing and refurbishing machinery makes perfect economic sense. Several consulting firms estimate this segment to be around $5.4 billion in 2026 and approximately $10.59 billion in 2030, although these figures should be approached cautiously as they stem from commercial reports rather than official sector statistics.

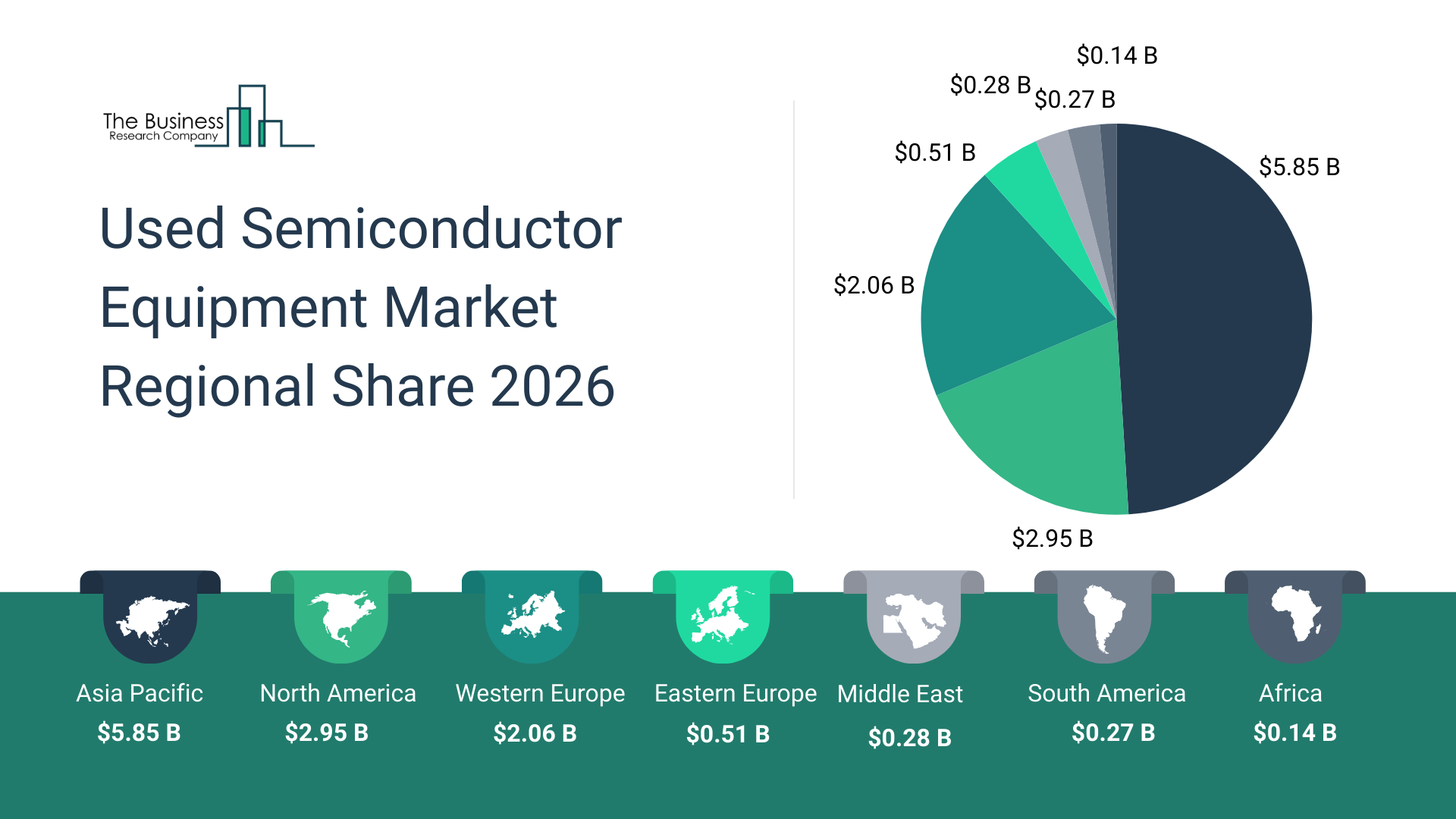

This caution is justified. Promotional material circulating recently about this market contains several notable inconsistencies: the announcement states $5.4 billion in 2026, but the associated infographic attributes $5.85 billion to Asia-Pacific alone, and summing all regions exceeds $12 billion. Similar discrepancies appear in the relative weight of the sector: if we consider a forecast of $196.07 billion for the global fabrication equipment market in 2030, a market of $10.59 billion in used machinery would represent slightly over 5%, not the 1% mentioned in promotional materials. Beyond these mismatches, the underlying trend aligns with the sector’s current state: WSTS predicts the global semiconductor market will approach $975 billion in 2026, and SEMI has been forecasting consecutive years of growth in equipment investment.

Why refurbished equipment is gaining ground

The rise of used machinery isn’t solely due to cost savings. It’s also linked to the actual structure of the industry. SEMI notes that investment in 200 mm factories continues to be driven by sustained demand for mature technologies, cost efficiencies, and supply chain diversification. Sectors such as automotive, industrial automation, or IoT continue to rely on this type of equipment to produce power semiconductors, MEMS, sensors, and analog circuits. In this realm, many tools from previous generations remain fully valid.

This explains why the second-hand market is no longer viewed as a marginal fringe. Often, these machines enable earlier production ramp-up, capacity expansion with less investment, or the preservation of plants still profitable for mature applications. For example, Lam Research markets its Reliant line for etching, deposition, and cleaning geared toward specialized technologies and nodes of 14 nm or higher, claiming it extends the productive life of fabs. KLA offers certified and remanufactured tools for 150 mm, 200 mm, and adaptable 200/300 mm configurations. Applied Materials emphasizes using refurbished parts whenever possible and designing systems for easier repair, upgrade, and reuse.

Even ASML, which produces the most sophisticated lithography equipment, acknowledges in its annual report that its installed base is growing not only with new systems but also with refurbished tools sourced by new owners, entering new markets and applications. The company sold 27 used lithography systems in 2025 and continues to update aging machines to improve performance and total cost of ownership over their lifespan.

A still-small business compared to new equipment markets

Despite optimistic forecasts, the used equipment market remains modest relative to new machinery. SEMI projected in 2025 that global manufacturing equipment sales would reach $125.5 billion that year and $138.1 billion in 2026, driven mainly by demand for AI, memory, and advanced logic. In this context, a $5.4 billion second-hand market would still account for less than 4% of the projected volume for new equipment in 2026. This means we are not looking at a replacement for the main market but rather a complementary layer that is becoming increasingly strategic.

The picture shifts somewhat when segment-specific data is considered. Commercial reports highlight photolithography, etching, deposition, ion implantation, and metrology as areas with the most second-hand activity. This makes sense: these are critical, expensive tool families with long lifecycles, where refurbishing can be much more attractive than waiting for a new tool—particularly for mature production, R&D, or specialized lines.

Asia leads, but the digital buy-sell market is also growing

Market studies agree that Asia-Pacific is the most dynamic region, with China emerging as a key hub due to its industrial capacity, foundry expansion, and self-sufficiency policies. However, beyond exact figures, what’s truly notable is how this market is becoming more professionalized. It’s no longer just traditional intermediaries or surplus inventory sold anonymously. Digital platforms specifically designed to provide liquidity, traceability, and greater visibility for the legacy tool pool are appearing.

SurplusGLOBAL introduced its SemiMarket platform at SEMICON Japan 2025, focused on legacy equipment and spares, offering real-time inventory search and AI-supported functions to match supply and demand. Meanwhile, Moov positions itself as a platform for buying and selling used semiconductor equipment, with additional services such as logistics, tracking, and documentation management. This digitalization enhances comparability, reduces friction in transactions, and increases buyer confidence.

Ultimately, this is what makes the story relevant. The used equipment market for chips will not displace leading manufacturers of new systems or the multibillion-dollar investments in cutting-edge nodes. However, it is establishing itself as a valuable tool for reducing deployment costs, accelerating capacity expansions, supporting production of mature technologies, and extending the lifespan of industrial assets with significant remaining potential. The opportunity exists, but some of the figures used to promote it still lack clarity, and further transparency would benefit the industry.

Frequently Asked Questions

What is the used semiconductor equipment market?

It involves buying, refurbishing, certifying, and supporting machinery already used in chip factories, including lithography, metrology, etching, deposition, or cleaning tools. This market primarily aims to expand capacity, set up specialized lines, or cut costs compared to purchasing new equipment.

Why are used tools still useful for chip manufacturing?

Because much of the global production doesn’t rely on cutting-edge nodes. Many automotive, sensor, power, industrial, and IoT applications are produced on mature processes and 200 mm fabs, where refurbished tools can remain entirely valid and cost-effective.

Do large industry players also work with refurbished machinery?

Yes. ASML, in its annual report, states that its installed base includes refurbished systems, and it sold 27 used lithography systems in 2025. KLA offers certified and remanufactured tools. Lam Research provides solutions to extend the life of mature fabs, and Applied Materials emphasizes using refurbished parts whenever possible.

Which regions are driving the used equipment market the most?

Commercial reports mainly point to Asia-Pacific due to its industrial weight and fabrications expansion. However, interest is also increasing in North America and Europe due to cost, resilience, and technological sovereignty considerations. SEMI highlights that supply chain diversification and public incentives continue to support investments in mature factories.

via: Press release